From 1 Property to 5: The Blueprint That Actually Works

One property done right beats five done wrong. Here's the roadmap.

Nobody builds a real estate portfolio overnight.

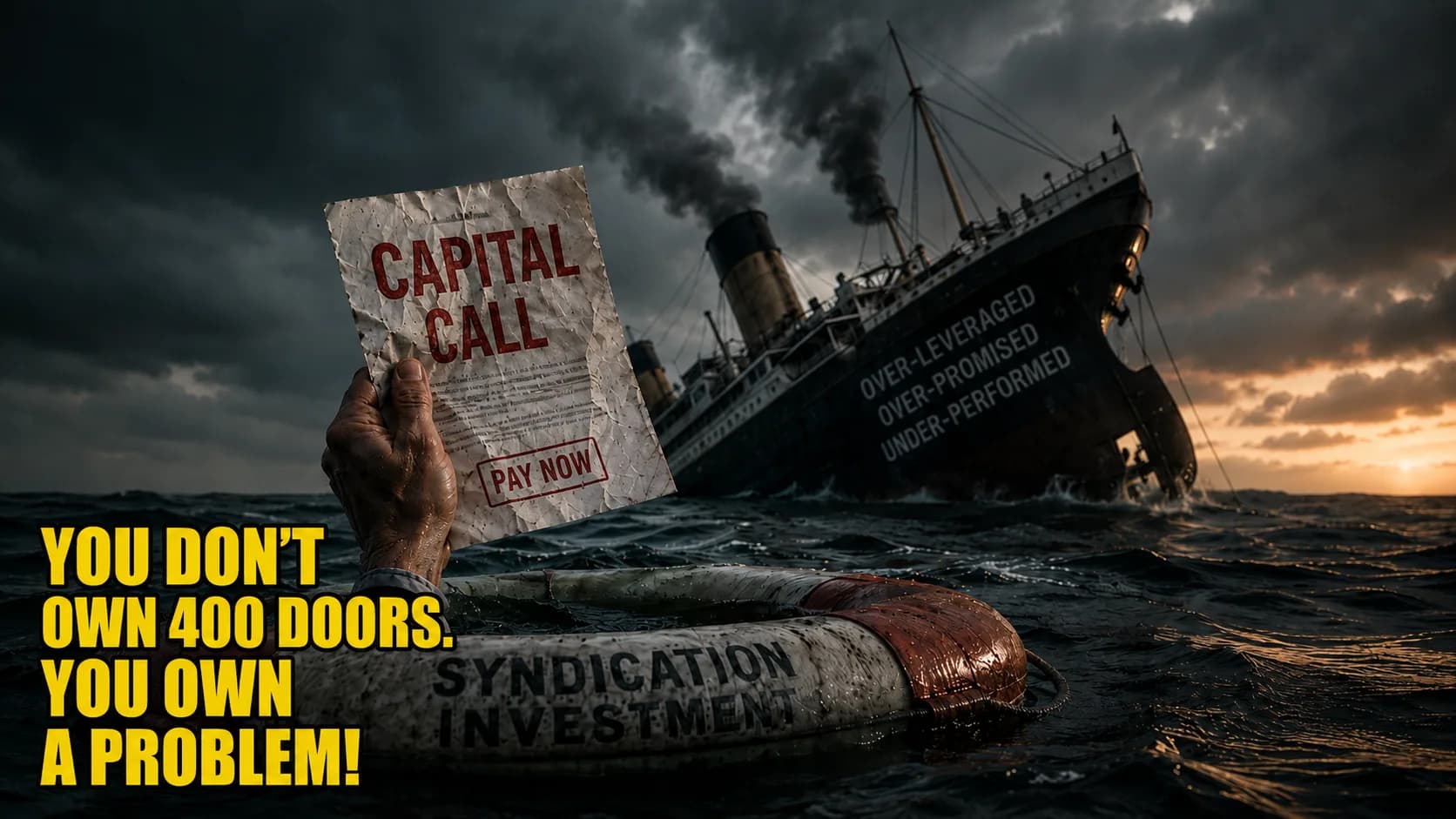

And the people who try, the ones who stack up five properties in 18 months on thin margins and floating rate debt, are the ones sending out cash call emails.

The right way is slower. And it works.

Here's the actual roadmap.

Years One and Two: Get Property One Right

This sounds obvious, but it's where most investors skip steps.

Buy your first property with equity built in. Make sure it cash flows. Get it rented to a qualified tenant. Get a manager you trust. Then let it sit.

Don't refinance it in month three.

Don't try to pull equity before you've made a year of payments.

Let it breathe.

Let the equity accumulate.

Let the tenant build your payment history for you.

The Whitmire property we've walked through throughout this series is a good example of what property one looks like. $40,000 in built-in equity, 7% cap rate, positive cash flow from day one.

Not exciting. Just solid.

Year Three: Use What You've Built

By year three, a few things have happened without you doing anything.

Your tenant has paid down roughly $8,000 to $10,000 of your mortgage principal. Your property has likely appreciated. Conservatively, 3% per year on a $269,000 market value property adds about $16,000 over two years. Add that to your original $40,000 in built-in equity and you're sitting on close to $65,000 in equity.

Now you have options.

A cash-out refinance lets you pull a portion of that equity out as cash, tax free, because it's a loan and not income, and use it as the down payment on property two. You've essentially let your first property fund your second one.

That's not a trick. That's just how equity works when you buy right and hold.

Properties Two Through Five

Each subsequent property follows the same framework.

Buy with equity.

Cash flow positive.

Quality market.

Let it accumulate.

The timeline compresses a little as you go because you have more properties appreciating, more principal being paid down, and more equity available to redeploy.

By the time you're working toward property five, the portfolio itself is doing most of the heavy lifting.

Five properties.

Each cash flowing $300 a month. That's $18,000 a year in passive income, plus five tenants paying down five mortgages, plus five properties appreciating.

All without you managing a single maintenance call.

The One Rule That Keeps It All Together

Every property has to stand on its own.

Don't buy property three hoping that property one's appreciation will bail it out.

Don't stretch on price because you really like the neighborhood.

Don't count on rent increases that haven't happened yet.

Each deal has to make sense the day you close on it.

Cap rate above 6.5%. Equity at purchase. Positive cash flow at current rent. If those three things are true, buy it. If they're not, wait for the one that is.

The investors who end up in trouble almost always bent this rule. Just once. That was enough.

More from Investing

All posts →

The Property Score That Killed The Sales Pitch

Most deals are dressed up. Here's the system we built to see through it.

Your Exit Strategy: Equity, Refinance, 1031, or Hold Forever

Most investors know how to get in. Almost none know how to get out.

They "Owned" 400 Doors. Now They're Getting a Cash Call.

One investor bragged about owning 400 doors. The other quietly closed on one single-family rental. Fast forward — one just got a cash call. Here's what the difference actually means.